Episode 308 – Working Class MMT with Bill Mitchell

FOLLOW THE SHOW

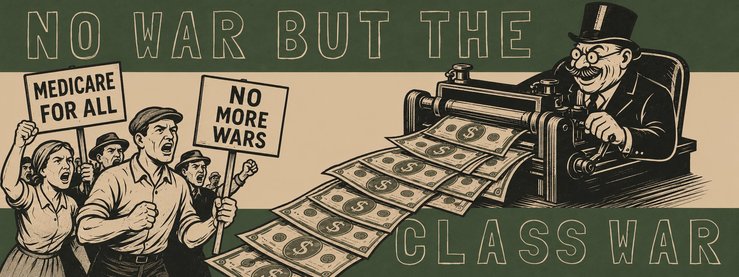

Economist Bill Mitchell talks with Steve about MMT and the importance of understanding the power mechanisms of class.

What’s the point of understanding money if we don’t look at the power relations controlling its distribution?

Bill Mitchell, a key figure in the development of modern monetary theory, is back for his twelfth appearance on the podcast, beginning with Episode One, Putting the T in MMT.

As a key figure in the development of MMT, Bill articulates how this theory fundamentally challenges conventional economic wisdom by asserting that governments, as currency issuers, are not financially constrained in the same manner as households or businesses.

This critical insight dispels the prevailing narrative that insists the government cannot afford to invest in social programs. This forces us to look not only at political choices, but the class power behind those choices.

The conversation delves into the dynamics of class conflict, inflation, and the role of private banks in shaping the financial landscape. Economic austerity, rising costs, and stagnant wages force the working class to take on more and more private debt.

Bill Mitchell is Professor of Economics and Director of the Centre of Full Employment and Equity (CofFEE) at the University of Newcastle, NSW Australia. He is also the Docent Professor of Global Political Economy at the University of Helsinki, Finland, and Guest International Professor at Kyoto University, Japan.

Bill is a professional musician and plays guitar with the Melbourne Reggae-Dub band – Pressure Drop.

Follow his work on https://billmitchell.org/blog/

Macro N Cheese Episode 308 – Working Class MMT with Bill Mitchell

December 21, 2024

Steve Grumbine

00:00:42.620 – 00:01:50.892

All right, folks, this is Steve with Macro N Cheese. I have been definitely hitting them out of the park the last couple weeks.

I’ve been really, really thrilled with some of the guests that we’ve had on. The topics we’ve had on have been timely. This is no different.

I am super excited to have my friend, genius, one of the best economists I’ve ever spoken to in my life, Professor Bill Mitchell joining me again today.

For those of you who do not know, Professor William Mitchell holds the Chair in Economics and is the Director of the Center of Full Employment and Equity {CofFEE), the official research center at the University of Newcastle, Australia. He also is the Docent professor in Global Political Economy at the University of Helsinki.

He is also a JSPS International Fellow at Kyoto University in Japan. He is one of the founders of modern monetary theory, and his blog is one of the leading economics blogs in the world.

With that, my guest, Bill Mitchell. Welcome to the show, sir.

Bill Mitchell

00:01:51.036 – 00:01:54.560

Yeah, thanks, Steve. I’m glad to be here, and thanks for the invitation.

Steve Grumbine

00:01:54.980 – 00:05:00.190

You better believe it. I mean, our last episode was really fantastic. It got a lot of listens, and I think people genuinely enjoy hearing from you.

Today is going to be no different, because I think that after 300, I don’t know what it’ll be by the time this is released, but as of this recording, we’ve got 304 podcasts of Macro N Cheese out the door. And you, sir, have done it multiple times, but you have the distinction of being podcast number one, and that is “Putting the T in MMT.”

And we talked about theory, we talked about understanding what a theory was, and it was one of our best episodes ever, folks. Most every one of our episodes, we try very hard to make them evergreen.

And that one, go back, listen to episode number one of Macro N Cheese, and you will learn so much. But today, what we’re hopefully going to be talking about in some detail is, you know, we’ve grown here at Macro N Cheese.

We’ve grown quite a bit, actually. And it’s been nice as we’ve tried desperately to incorporate a class awareness, class consciousness into our discussion points.

And so as a result of that, what we have done is we have approached each and every one of these episodes with the intention of changing the focus, changing the lens so that the focus is no longer on the investor grade people, the investors, the PMC [professional managerial class]. We’re looking at the working class. And the majority of the people around the world make up the working class.

It’s a very, very small group of people that don’t make up the working class. And they’re often the least talked about and talked to.

And they have very few people that speak for them or even try to translate the information we hear so that it’s meant for them.

So what I’ve asked Bill to do today is to kind of take us through a trip on modern monetary theory [MMT] with a focus on the working class and really get a feel for some of the things that, you know, I know a lot of socialists have come to Bill and said, hey, that’s not, you know, that’s not right, or hey, you know. And Bill is one of the guys that really does get class.

Last time we talked, he talked about straight up that his background came from Marx and Michał Kalecki and so many other voices from the left. And Bill wrote many great books. One of them in particular is called Reclaiming the State, a very important book.

If you haven’t read it recently, he co-wrote it with Thomas Fazi as well, please go out and get that book. But for this conversation, it’s going to be bringing it back to basics.

So, Bill, you know, I’ve been trying my best to come up with a different way of saying this stuff over and over and over the last decade. Sometimes I get it right, sometimes I get it wrong. How would you describe modern monetary theory to someone from the working class?

In this era of Trump, in this era where the working class is repeatedly ignored, how would you define and describe modern monetary theory?

Bill Mitchell

00:05:00.610 – 00:18:08.800

You know, the way I see the world is that there’s these complex layers of power relations, and these are sort of political lobbying. They’re essentially class layers.

And what I mean by class, of course, and I’m not talking here about middle class or upper class or lower class, I’m talking about economic class in the way in which Karl Marx originally conceived the concept, the breakdown of society.

Breaking it down into classes, not breaking it up, is that our starting point to understand how the system works, the power relations within the system, should be to understand that one sector in the economy, in our society. Now, society and economy aren’t equivalent. One segment is owning what we call a material means of production, that is capital.

Now, in the industrial area that was productive capital, machinery and equipment and assembly lines, and even back earlier, spinning jennies in factories. And it’s become more complex because we’ve now got this sort of whole overlay of finance capital, which is another sort of power line.

So one section owns the material means of production.

And in other words, they don’t have to work personally to generate income, but what they have to do is hire the other broad economic class, the working class, to work with that capital.

And the way in which the capital owning class makes a living through the industrial relations of our economy is to force the working class to work for more hours in a day and produce more things in a day than the workers strictly need to fulfill what we think of as their subsistence needs. In other words, subsistence doesn’t mean bare existence, it means what we need to survive in this society.

Food, shelter, clothing, entertainment, whatever. And so by being able to coerce, coerced doesn’t necessarily mean with a whip.

It means using power relations in the economy by coercing those workers and forcing them to work longer than they strictly need to to cover their own subsistence. The capital owning class then can expropriate what we call the surplus value produced.

And as long as they can realize that surplus value as profit by selling it into the goods market for a profit, in other words, price above cost, then they generate an income without having to work. And the big distinction is that the working class accept that coercion, albeit reluctantly, because they’ve got no choice.

They have to work to survive, to get an income, because they don’t own capital independently. Now that’s the raw bones of the power relationship.

And it gets much more complex then when we add layers, like the middle class and the professional managerial class. You know, I’m in the professional managerial class as a professor, but of course I’m still part of the working class because I don’t have capital.

But there’s much more complicated dynamics then.

But the essential point, the starting point that I have of understanding the power relations in the economy is that those two broad economic classes are in conflict with each other. And the nature of the conflict can be summarized in the most simple way.

That the owners of capital want the working class to work as long as possible and pay them as little as possible, because that way they can maximize the surplus value each day that they get out of each worker.

Whereas the alternative ambition for the working class is that they want to work for as short a time possible, with less intensity, and get paid the most. So you juxtapose those two positions and you can easily see that there’s a conflict.

Now, once you start understanding that, starting from that point, then you can understand the dynamics of organizations, the control and supervision structures of management, the complex divide and conquer strategies that capital employ to ensure that the working class doesn’t unite as a whole. And so some of the strategies are to exploit identity, gender, race, poverty.

All of these types of things are used to create the impression that there isn’t an homogenous working class. So that’s the first element in the way I understand the world. Then we come to the monetary system, which is an aspect of the economic system.

And this is where modern monetary theory comes in.

Because to understand what we call a fiat currency system now, that just means that the monetary system is introduced as a legislative fiat by the government, the currency issuing government.

And the distinction you make is that in former eras we had examples of commodity monetary systems which were like gold or silver coins, for example, and the currency had intrinsic value because of the value of the commodity, the metal in that case.

Whereas the distinction with the fiat currency system is that the fiat currency are just worthless tokens until they are brought into use by government through the imposition of an exclusive imposition of a tax liability that has to be relinquished through that currency. And that’s what gives this worthless token value, because we then have to get it, and we don’t have it until the government spends it.

Now, a lot of people, almost everybody, has been led to believe that the government, like the US Government, spends taxpayer’s money. Now the reality is that how can that possibly be so? Because the US Government is the one that issues the currency, it’s their currency.

And the US taxpayers don’t have that currency until the government spends it. Just a logical temporal set of reasoning. You can’t get the currency until it’s been spent.

And that should militate against thinking that the taxpayers are funding the government spending.

Now, modern monetary theory is a way, a superior way, of understanding the operations of the fiat monetary system and the capacities of the currency issuing government and the consequences of using that capacity.

So juxtapose that with, say, mainstream monetary theory, which starts with the presumption that a government is financially constrained like a household, and therefore has to seek sources of revenue in order to spend.

And then there’s a whole narrative built on the evils of taxation and the evils of issuing government debt and the inflationary consequences of spending in excess of those sources of revenue.

And you juxtapose that with MMT that says, well look, the US government can’t possibly be financially constrained unless it voluntarily brings in rules to constrain itself [e.g. the debt ceiling]. It can’t intrinsically be financially constrained.

And so therefore you’ve got to investigate, well, what’s the role of taxation, why do such governments issue debt? And questions like that.

And what you find once you start teasing those questions out is that modern monetary theory provides a totally at odds explanation and understanding of the way in which the monetary system operates, the way in which the institutions like the banking sector operates, the capacities available to government, and the consequences of using those capacities. Now then, put those two things that I’ve just discussed briefly, the power relations together with the monetary understanding.

And this is the last point I’m making as my first response to you is a lot of people get confused when they first confront modern monetary theory and say, oh well, if we don’t like it, you know, it’ll be dangerous, et cetera, et cetera.

And others perhaps with a more progressive bent or saying, oh God, we love this, you know, we can have hospitals and public schools and we can look after the environment and we can have transport systems and all the rest of it. And of course they’re both wrong because that understanding of the monetary system doesn’t really have any policy structures. And go back to that.

The people who think it’s a regime, it’s neither left nor right, so it’s neither progressive or any ideological position on the continuum. And a lot of people really get this wrong.

They sometimes hear me talk and I’m on the left and they say, oh well, the MMT must be left, whereas it’s not.

But the point I make is that, you know, I’m looking at my computer screen now with my glasses on because otherwise I can’t see very well, given my aging eyes.

And MMT is a set of lenses to allow us to really investigate and drill into the monetary system and understand the sort of dynamics of those institutions and the way it works.

That understanding gives us a much better feel for what would happen if governments did A or B and cures us of the fictional blinders that mainstream theory, which really doesn’t give us any understanding. Now to activate that understanding into a policy space, you need to impose your set of values, your ideology.

Now, a person on the extreme right could have exactly the same understanding of the monetary system as me.

In other words, be an MMT-er, that they would use that understanding to advocate for free market policies, you know, corporate handouts, whatever, whereas a person on the left would use that understanding to say, well, we can have better schools, better public transport and those sort of things. And they both share the understanding but have polar opposite policy spaces.

And that’s the point, that it’s not a ideology or a regime that you move into or you can move out of.

It describes the currency systems that we have in place today in your country, the US in my country at the moment, Australia, in Japan, in all over the place. Now then, the last step of the question is to form an understanding of why the government uses its currency capacity in particular ways.

In other words, what influences the government’s decisions? And that’s why you need a class analysis.

Because unless you can understand the context, the power context in which governments are embedded and influenced by, you can’t really get a feel for the likelihood of one policy set after another.

So I think that the complete picture for a person wanting to understand how the economy works is to have a good class analysis basis, a good understanding of class which leads you to interrogate power relationships and all of the obfuscating layers that those power relations trigger to hide them, make them less transparent to everybody.

And you also need to have a very solid understanding of modern monetary theory so that you can then understand the consequences of governments using different policy tools that have been driven by the way in which the power relations drive it. So that’s sort of big picture, nothing particularly specific, but that’s the way I think of the economy. Now, many MMT-ers don’t think like that.

They don’t include the class and the power element in a broad explanation.

You don’t need the class element to understand the mechanics of MMT, but you need the class element to understand how the government is manipulated into doing one thing or the other.

Steve Grumbine

00:18:09.660 – 00:18:35.840

That’s very, very well said.

And one of the things that was intriguing to me, and now mind you, this has been said by several people, so I don’t know who to give credit or blame to. Okay, but one of the things that has often been said is that money does not exist within the government sector.

That money only exists once it’s spent into the economy and the private sector. When I think about that, first of all, let me ask you, is that a true statement?

Bill Mitchell

00:18:36.140 – 00:18:44.960

Well, I mean, what’s the point of the statement? That’s the question I would have. What’s trying to be elucidated by saying something like that?

Steve Grumbine

00:18:45.260 – 00:19:05.398

Well, I guess the point of it is that once it leaves government, it’s no longer neutral. It’s now been spent on something that had a political or a class angle, a class interest, a policy because government spends money into existence.

Bill Mitchell

00:19:05.454 – 00:19:08.850

There’s no problem with that. But what problem are you thinking about here?

Steve Grumbine

00:19:09.150 – 00:19:43.522

Well, I think I’m looking at it from a standpoint of when we talk about MMT in the theoretical framework, in its very academic sense, it oftentimes leaves people wondering.

Well, hold on, if it’s neutral, then how come once it’s spent into the economy, it stopped being neutral the minute that Congress passed a law, the minute that Parliament passed a law, the minute whoever it was that via whatever legal framework they have to get it out there, someone’s class interests are immediately dealt with once it is out of the government sector.

Bill Mitchell

00:19:43.626 – 00:19:46.590

Of course there’s no problem with that.

Steve Grumbine

00:19:47.050 – 00:21:01.520

So from a person on the left, and I’m trying to be representative of some of the questions that come my way in this space, they don’t understand that you’ve basically framed it in the first answer. But within this commentary here, right, it’s like, well, MMT, once you spend it, we stopped just dealing with the base case.

Now we’re talking about the values. We’ve entered the values almost immediately.

Once money came to be, when a leftist or when a working class individual, maybe it’s not a leftist, maybe it’s just a regular working class person that doesn’t have a developed theory of values from a standpoint of a sophisticated school of thought.

Maybe they’re just a rank and file human being that sits there, goes to work nine to five, comes home, eats dinner with the family maybe and turns on the TV and starts hearing the news, which tells them all kinds of lies nonstop. I guess that’s first problem right there. But when they hear this stuff from an MMT perspective, where does the class kick in?

When should someone’s ears perk up that understand the government as the currency issuer, when should they start really paying attention to the values?

Bill Mitchell

00:21:01.680 – 00:26:06.130

Yeah, fine, I sort of get where you’re going. I mean, anything the government does is ideological and political, obviously, because they’re politicians and that’s their business.

So take two really quite extremely different examples. Yeah, you can be controversial here. Think about the current terrible state in Gaza and the US government’s involvement in that.

Now I’m on the public record of saying that the key to that conflict is the US Government because it could force the Israelis into a negotiating position by stopping funding their slaughter. So that’s quite clear.

You know, it’s hard to get your head around how the billions of dollars that are flying into Gaza from rockets and weapons every hour of every day, the billions of US dollars that are just flying through the sky and destroying communities and killing people.

Now from an MMT perspective, the insight you get is that, okay, the US can obviously never run out of the US dollars to fund the military industrial complex to produce these weapons and generate profit through procurement contracts, can never run out of the US dollars. And there’s no question about that.

So the Gaza issue becomes not a, from an MMT economist perspective isn’t about how do you pay for all of that, isn’t about the government will run out of money if it’s doing that. The question then is, well, is that the best use of the currency issuing capacity of the US government?

Now obviously the dominant majority thinks it is because it’s happening. That’s the political aspect, the power aspect, the lobbying aspect. Whereas I think it’s the worst use of US dollars that you could ever imagine.

Now then, take another example.

And we might think of it as improving poverty in some of the ghettos in Los Angeles or in Baltimore, some American cities that cease to work as a healthy environment for people to live in. There’s all sorts of things that social welfare and urban designers would advocate to improve housing.

And you could ally this with environmental sustainability ambitions.

You know, improve the quality of housing so that they’re more energy efficient and sustainable, provide better community facilities so that children don’t grow up with a sense of hopelessness, provide guaranteed employment to kids who are falling out of the education and training system and you know, all the things that would improve the health and welfare of those very disadvantaged communities. And why isn’t it being done?

Well, mostly it’s not being done because the government has been lobbied to tell citizens that, oh, we can’t have everything because we don’t have enough money. And if we tried to do that, there’d be inflation or there’d be higher taxes and we’d run out of money.

Now what an MMT economist immediately says, well, in the same way you can never run out of spending money on military equipment, you can’t run out of money on helping poor communities improve their material circumstances a little bit, can never run out of their money.

And so the question as to why you’re not doing it is because your ideology doesn’t want you to do it, not because you don’t have the financial capacity. The reason you’re facilitating the bombing of Gaza and not improving the drug-addled areas in Baltimore is because you’ve chosen to do that.

And I think that’s the juxtaposition that citizens need to start thinking about. They should never buy the argument, oh, the governments can’t afford this.

Well, it might be that at certain points in history you couldn’t afford to do anything like improve housing in Baltimore, for example, because there wouldn’t be enough carpenters available, in which case you’d have to take a longer term perspective. That would be the constraint.

But the message of MMT is that all of those diversions about how to pay for something and the government will run out of money and that we can’t afford it, they’re all diversions to hide an ideological commitment to something that is likely to be unpalatable to many people.

And so I think the working class of America should get their heads around the fact that they’re being kept in an increasingly impoverished state with failed communities and intergenerational disadvantage being inherited, while the US government has all the resources it needs to reverse those things. But it’s choosing not to do that.

And it’s also choosing to use some of its infinite financial resources to kill the most disadvantaged people in Gaza. I think they’re the sort of juxtapositions that people should get their heads around.

Steve Grumbine

00:26:06.670 – 00:26:27.206

That’s perfect. I was trying to drive towards that once government spends this stuff into existence, whether you like it or not, it’s never an issue of solvency.

No, it’s always an issue of priority. It’s always your values coming into play once it leaves the government sector, once they spend it into existence.

Someone’s values were represented right there.

Bill Mitchell

00:26:27.278 – 00:26:27.958

Absolutely.

Steve Grumbine

00:26:28.054 – 00:27:43.378

And those values frequently, if not almost always, are not in favor of the working class. In fact, the working class is led to believe every election cycle that these politicians are going to do something wonderful for them.

And they didn’t even try to do that this past election. That’s how bad it’s got. They didn’t even try to sell anybody anything. It was just, hey, you know, you don’t want this guy over there or whatever.

And we witnessed the genocide that you were addressing there. And there was a lot of reasons why people swung a certain way in the election. Most of them economic.

And you know, as I think to myself, when I started paying attention to MMT, I did not come to MMT because, oh, isn’t this just something neat? Cause I just love math and I liked formulas and I liked, you know, economics. In fact, I did okay.

I got through grad school, but I wasn’t an all star at this stuff and I learned all the wrong stuff. It was when my values kicked in and I immediately saw that I was fighting stupid battles. I was fighting battles that weren’t real.

And that really irritated me. And I think that’s what’s kept me going for 15 years. I’ve been doing this stuff since 2007. So I guess 17 years.

Bill Mitchell

00:27:43.514 – 00:27:44.550

Amazing.

Steve Grumbine

00:27:45.290 – 00:29:32.332

Just a dork doing it for 17 years. What is wrong with me? But for 17 years it’s been in my craw. And for 17 years, my purpose was my values first.

I led with my values and I saw this as a tool. I saw this as a framework for taking the things I valued and bringing them to fruition and helping others see that they were possible.

And I don’t know what it is, but at some point it just hit me like a ton of bricks and I haven’t been able to get off the horse since.

But with what you’re saying here, you know, there’s a lot of things that come up in the news that people hear and like most people that are not well informed, they just run with whatever the narrative is. And I want to throw a few very important narratives out there right now that kind of play into the base of MMT and also from a class perspective.

You know, we talk about how they cry poor mouth when it comes to helping the poor, when it comes to making the environment better, when it comes to structural changes that would literally free the working class of the burden of the sack, as they say, you know, the freedom of the fears of being laid off. But that fear is a ideological desire to train the working class how to be.

And so as I think to myself about bonds, for example, you know, they’re always talking about, well, what if they lose faith in the dollar? What if they stop buying your bonds, Then what? And I laugh and I think, well, Japan sure likes to buy their bonds.

The US likes to buy their own bonds too. Almost every government around the world buys their own bonds up when they’re not purchased by someone else.

Help me understand the role of bonds in the MMT lens. Bonds, gilts, whatever you want to call them.

Bill Mitchell

00:29:32.516 – 00:33:53.020

Well, I mean, the first point to understand is that once you accept the notion that the currency issuing government, like the US government, has no financial constraint, then the concept of having to get its own currency from the non-government sector by selling debt instruments–bonds–just becomes absurd. So the mainstream theory says, oh well, the government’s got a financial constraint, therefore it’s got to raise money by tax.

And if it wants to spend more than it raises money from tax, it really has to then go into debt. Now that perfectly describes a household like you and me that if we want to spend, we have to find a source of income.

And if we want to spend more than our current earned income from our work, then we can run down prior savings or we can sell assets on ebay, or if we want to buy big things like a house, we have to go to a bank and get a mortgage. So it’s quite clear that that’s the behavior and the financial constraints on a household.

But then trying to suggest that those constraints carry over to the government that has its own currency and issues it, is one of the greatest con jobs in history of the academy. It’s just totally untrue and improbable if you think about it. So then you think about, well, why does the government issue debt?

Why is it borrowing money from the non government sector if it doesn’t need that money in order to spend? And the answer is varied. The essential point that I want to make is that it doesn’t need that currency in order to spend.

That’s the first point to really get clear. Warren Mosler and myself started all this. We’ve advocated that the government just should stop issuing debt altogether.

There’s no value function in it. But when you think about, well, what happens when it issues debt?

Well, it’s providing a risk free asset to the non-government sector to park some of their savings, some of their wealth they’ve built up in a risk-free asset. Whereas all financial assets that are issued by non-government bodies like banks, corporations, you know, whatever, they’re all risky.

But the debt that’s issued by the US government, for example, or any currency issuing government has no risk, no financial or credit risk. There’s no reasonable prospect to assume that such a government would ever default on its liabilities. Why?

Because it can always fund its liabilities because it’s got its own currency. So then the question is, what are the consequences of it issuing debt? And we’re back into the value territory.

And the question is, well, whose ambitions does it serve for the government to be issuing debt? Well, the answer is quite clear, that it serves the corporate interests. I call it corporate welfare.

And the reason I say that is because it provides the speculators in the financial markets who add no substantive value to the wellbeing of our communities. They’re the most unproductive sector in the economy.

It provides them with a risk free benchmark upon which they can price their other more risky financial assets. So as a benchmark. And it also gives them a safe haven when the speculative environment becomes very uncertain.

And so when you have financial turmoil and it’s not clear, that there’s companies going broke and the corporate bills are defaulting.

For example, the existence of government bonds provides a safe haven for corporate speculators to shift their funds into a risk free asset which might have a lower return, but is risk free. It’s safe away from higher, riskier assets that are very uncertain. And the speculators form the view that they may well lose their funds.

So it’s just corporate welfare and totally unnecessary. Governments around the world should just stop issuing debt.

Intermission

00:33:54.000 – 00:34:17.372

You are listening to Macro N Cheese, a podcast by Real Progressives. We are a 501c3 nonprofit organization. All donations are tax deductible.

Please consider becoming a monthly donor on Patreon, Substack, or our website realprogressives.org. Now back to the podcast.

Steve Grumbine

00:34:17.396 – 00:34:43.212

So when you think about the money that’s paid on the interest, most working class people are saying, hey, that’s my hard earned tax dollars going to give those people that money that I have to pay off that debt. And in reality that’s not true at all. That’s actually new money being spent based on a value system.

The interest on that stuff is new money spent into the economy, spent into their bank accounts. Is that correct?

Bill Mitchell

00:34:43.276 – 00:36:58.890

Yeah. I mean the government is providing an income source for those who hold financial assets.

Now the ideological perspective or aspect of that statement is to ask, well, what’s the distributional implications of that? Who’s getting this income? There’s no question the government can fund that income at any point in time.

The question that should be asked is, well, who’s benefiting from that whole system? Now in the sense that I call it corporate welfare, I’m immediately telling you who’s benefiting. It’s not the working class because they tend not to hold those sort of assets.

Now it gets complicated and remember, go back to the beginning of today by these multiple layers erected on top of the pure class layer.

So you know, the middle class who are part of the working funnel have been extracted more through mass education, et cetera, into the professional managerial class.

They become a sort of schizophrenic class because they’re part of the working class, but they serve the interests of management above the pure interests of the poor and the unskilled workers. And that complication then says that they have pension funds. You call them in America, we call them superannuation funds, but the same thing.

And those superannuation funds extract savings from workers which they then invest in government bonds through various regulations on safety of their pension funds. So they also buy bonds. Now if we scrap bonds, what would be the consequences for the workers who have invested in those, the middle class workers?

Well, there would have to be some other safe asset. Now my response to that as a member of the working class is that the government should, and always can, set up national pension funds.

We don’t have to have private for profit speculative pension funds. We can have government provided pension funds which benefit everybody and which could never go broke.

You don’t then, in other words, have to have a debt issuing machinery to provide that sort of safe asset for workers savings.

Steve Grumbine

00:36:59.390 – 00:39:27.182

And there you go.

I mean, we have in the US Social Security and many people end up living on Social Security and they have been convinced that because government can go broke, because the trust fund can go broke, et cetera, that they should privatize this. And now with this new regime coming through, Trump and his friends Musk and Ramaswamy, they’re looking to take a scalpel out and cut everything off.

I mean, forget a scalpel, they’re looking for a chainsaw. They’re ready to take huge agencies and just throw them into the dustbin.

And maybe that’s good in some cases, but it’s not in the interest of the working class in particular.

But because the working class has been so duped into believing that government is broke and it’s their tax dollars being wasted on these stupid agencies, not realizing once again it’s an ideological thing, the government has chosen to fund those things up to this point. And that is new money. That’s not tax money.

That is new money being spent by the government on those things, which provides many, many families, children, you name it, lots of benefits, lots of good quality of life, et cetera. But because they have been convinced that Social Security can go broke, they want to privatize it.

Because they convinced that these agencies are sucking away taxpayer dollars and your hard earned tax dollars getting wasted on government largesse. They have been convinced of this. So they’re out there ignorantly bleeding and begging for this.

And as a working class individual, I’m horrified that this is what we’re up against, to get our own people to have the values that they think they have, but really the right values because they understand how the system works.

When you say that government could provide debt free pensions where they don’t have to sit there and worry about bondholders and this, and they could just simply fund whatever age they want to pick, they could say from cradle to grave, or they could say from 50 to 100, whatever, but that again is a value that’s not a financial constraint. That’s not an issue that the currency issuing government could not achieve.

So they are diminished by this lie that is perpetuated by both Democrats and Republicans in the United States, Tories and Labour in the UK and I’m sure all the Greens and everyone else in Australia, I don’t think any of them get it right, do they?

Bill Mitchell

00:39:27.366 – 00:42:02.690

Well, look, you know, in Australia, for example, we have a broad aged pension system that’s just totally funded by government.

Now if you’re in the higher income groups and you are members of private pension funds or superannuation funds, well then it may be that you generate too much income potential to receive the government pension. And that’s certainly the case.

There’s no question that the Australian government as the currency issuer can always provide an aged pension at a reasonable rate. It’s not too bad actually in material terms, there’s no question about it. So our system is somewhat different to the US system.

But yeah, I mean the US Social Security trust fund issue has been around for years and there’s been a whole conga line of economists predicting it’ll go broke.

And you know, every few years you’ll get them coming out and as new graduates get their PhDs, they get the media voice and they predict it’ll go broke too. It can never go broke unless the government allows it to. It certainly could go broke if it becomes privatized.

We’ve seen the folly of privatised enterprises since the mid-80s. They sometimes go broke and they need rebalance from government again. But the U.S. Social Security system can never go broke.

And the only question that people should ask of that is not their dollars aren’t funding it, it’s the US government’s dollars that are funding the government’s contribution that can never run out of money. The only question is, is it generous enough?

Is it providing necessary material support for people who own either too old to work, too infirm to work, or otherwise disabled? And that’s the only questions people should ask. Is it serving that purpose? The purpose of the trust fund is that.

But the debate in America is diverted into these ridiculous questions. Oh, it’s going to run out of money.

And you get these economists who pretend they’re very erudite and produce graphs showing when it’s going to intersect the solvency threshold. It’s just a lot of nonsense.

I never see any of these economists saying, well, when’s the government going to run out of money to fund Israeli Defence Forces?

I never see them say that yet the scale of the investment in that venture, that disgusting venture, is massive compared to the sort of scraps they hand out to disadvantaged communities.

Steve Grumbine

00:42:03.750 – 00:44:10.370

So the thing that always comes up at this point in time and even when you go to AI and you say AI, tell me what MMT is, right, it does pull some of you guys’s brain trust, but it pulls a lot of nonsense in there too. And at the end it says things to worry about with MMT.

And this is, well, if the government spends too much money, you could have spiraling inflation, okay? And I laugh to myself because this is the kind of fear porn that is sold to the working class. So they’re afraid to ask for anything.

They’re terrified that their taxes will go up to pay for it. They’re terrified that if the government spends money into the economy, which does every stinking second, that it’s going to create inflation.

And I know MMT has always centered inflation as a real legitimate constraint.

But you know, what we experienced here recently during COVID and currently now coming out of it is people are still suffering majorly from inflation here in the United States because wages did not go up with the cost of living. And as a result of that, you know, one man’s spending is another man’s income. The working class is getting gouged again.

And we’re finding through various people’s work that it is not just some fact of the government choosing to pay higher prices. There were signals sent to industry that the government’s spending money and they responded by hiking up prices.

And there were some businesses that were seen to have gouged up to a thousand percent profit over that period of time.

And so they, rather than asking their government to do price controls or have anti-gouging laws or go after the smoky rooms where those people are incentivized to maximize shareholder value instead to maximize the well being of the working class or well being of the entire country or anything. So you never think about that. So Bill, from an MMT perspective, can you define what inflation is and isn’t and how it comes to be?

Bill Mitchell

00:44:10.750 – 00:50:39.820

Well, look, that’s a difficult question, but the most basic understanding is that all spending in the economy carries an inflation risk.

Whether it be household consumption spending, whether it be business investment on machinery and equipment or infrastructure, whether it be export sales, which is foreign spending coming into your economy, or government spending. There’s nothing exclusive about government spending in this context.

And what that risk is, it applies to all spending components, is that if the nominal spending, that’s the dollar value of the spending grows in excess of the capacity of the supply side of the economy, that’s the productive side to respond by producing goods and services in response to that spending. Then you’ll start getting inflationary pressures, which we attribute to being excessive demand, excessive spending.

Now, the problem is that that’s a relatively simplistic view of the inflationary process because once you start thinking in class terms, then you start to understand that inflation can also emerge out of the intrinsic class conflict between labor and capital.

And you know, the classic example is the 1970s when as a consequence of the Saudi response to the Yom Kippur War, which was again, the Israelis sort of trying to illegally take land off the Palestinians and were being supported financially and militarily by the US Government, the oil producers decided to punish the US by increasing the price of oil, dramatic doubled overnight, almost October 1973. And if you then think about, well, what does that mean?

Well, it means that all oil dependent countries were immediately faced with a massive increase in imported raw material costs. Raw materials that are dependent upon oil to run their economies.

And the question then for the economy is, well, in terms of how much you’re producing any particular time, is that in real terms now you’ve got less income to distribute domestically because an increasing proportion of the income you’re producing has to go to the rest of the world to fund the higher price for the imported raw material, in this case oil. And so once you start asking the question, well, how is that real income loss going to be redistributed? Who’s going to take the real income loss?

Well, then you’ve got class dynamics.

So are the workers going to take it in the form of lower real wages, lower purchasing power, or are the bosses going to take it in the form of lower real profit margins, or are they going to share it or what?

And what we saw in the 1970s is that trade unions at that stage were much stronger than they are now and had the capacity to resist the real wage cuts coming from the higher prices as the raw material price escalation was being passed on.

And the corporations have price setting power, obviously, because it’s not a free market out there. They’ve got power to manipulate and set prices.

And so you had a distributional battle where the working class would push up nominal wage demands as the prices were rising in order to maintain some real wage target. And the owners of capital were trying to maintain a real target rate of profit, a margin, in other words.

And so they would retaliate if there was industrial action trying to push higher money wages to get this real wage target. And the price setters in the corporations would then push the prices up because their cost structure had now risen.

And so you had an inflationary spiral emerging out of a distributional struggle, a conflict over who was going to take the losses of the raw material price rises.

Now to some extent, COVID was a replay of that with a major difference as the supply constraints were emerging and people were ill, and factories were being closed and shipping was being disrupted and governments were forcing people to stay at home because they hadn’t quite worked out how we’re going to deal with this unknown threat. The question then was, well, who was going to take the losses?

And the corporations soon worked out that their trade unions were now so weak that they weren’t going to resist.

And so the price inflation that emerged from that supply side constraints drove the real wages of the workers down systematically because they couldn’t resist them anymore. And then of course, many corporations who had price setting power worked out, well, you know, we’ve got a party on here.

We can really take advantage of this power imbalance and not only defend the margins from the increased costs of production from the supply constraints, but expand our margins and therefore expand our real profit margin. And that’s what they did.

The inflation persisted and amplified by the fact that corporations all around the world, not just in the US, in Australia, not everywhere, most places, took advantage of their price setting power, their lack of competitiveness within their segment, the productive segment, took advantage of that and went crazy. And the way in which the policymakers responded was to assume it was just a simple excess demand case, the case I made in the beginning.

And that’s why they started to push interest rates up. That was their avowed justification.

But really the problem was the transitory constraints from the supply side or from the productive side arising from COVID and then Ukraine and OPEC [Organization of Petroleum Exporting Countries].

But on top of that, this price gouging you mentioned, because the imbalance between unions and corporations and all of those things were really not sensitive to interest rate changes, which meant the monetary policy changes that occurred were a total farce.

Steve Grumbine

00:50:40.880 – 00:53:03.710

I want to take us down two quick paths before we close out Bill. And by the way, thank you so much for your time. The last one I guess is a two parter, so we’ll make it one here.

You know, people are looking around for ways of surviving this.

My family, we have a special needs child, and we’re watching the government threaten to strip away services for special needs kids, and services across the board.

And so people are looking into different asset classes to try to gamble what little savings they may have, to try to get ahead of it to protect their families. And so you’ve got the rise of crypto[currency] and people see this as hey…

In fact, some of the comments we get back to some of our substack posts about MMT are this is an old thinking, this is old money thinking, this isn’t real, this is old money. You’ve been bypassed by crypto, guys, you’re crazy.

And so the vast majority of working class people, those who do have some money and those who don’t have some money, are looking at crypto as a way out and they’re thinking that this will kill the monetary system. And the second part to that is the role of private banks in terms of how people see money.

The combination of going in debt by taking out loans as opposed to buying this crypto. Two questions, one theme. They’re scrambled and they’re trying to find a way out, either via loans or via speculative assets like crypto.

I guess question number one is, is that just because crypto is something that people invest in, doesn’t mean that it makes the old monetary system null and void. In fact, I would suggest that it’s built on top of it.

And the other thing is that the idea of private banks creating all this money, this is typically thrown at us in the same way. And they use this as their reason why they’re buying crypto, because after all, they’re diluting the value of the dollar and so forth.

But the role of private banks in lending, I mean, this is a policy, this is once again a value discussion. Am I correct in that?

I mean, the reason for private banks, as opposed to just having everything centralized through the government, is a policy decision. It’s a value system that they would rather do.

And so when you take out private debt, that’s real debt, you gotta pay back when the government spends it on you. That’s not the same thing. Can you elucidate on both of those points?

Bill Mitchell

00:53:04.010 – 00:58:18.466

Well, look, I think there’s been overblown ambitions for cryptocurrencies. They’re never going to replace the currency of the state. They’ve made some people very well off and they’ve made many others desperately not well off.

And I guess what I would say is that the vast majority of the working class in America are not in a financial position to speculate in financial markets per se, and certainly not in cryptocurrency markets. The data suggests that they don’t even have very good pension entitlement buildups and savings. The vast majority of Americans don’t have any savings.

And certainly the hollowing out of the middle class over the last 30 years has meant that more and more Americans are in the lower income category with very constrained financial asset holdings. Now, many of those people voted for Donald Trump. And I think that most voting is on emotion.

And when you then add an economic component to it, it’s also built around the mainstream fictions that we’ve talked about. And going back to earlier on in our discussion, that’s one of the reasons why I think modern monetary theory is valuable.

In my view, it will provide an increased quality to our democracies because the sort of questions we’ll ask politicians and the sort of answers we’ll be prepared to accept change dramatically. An MMT framework leads a person to reject outright statements like we can’t afford that because we’ll run out of money or you’ll have to pay higher taxes. It forces us to change our focus to real resource availability.

And then that says, well, how are we going to generate skills in the future when we need investment in training systems? Not that we can’t afford them, but we need them.

So there’s all these different questions and answers come up which would improve the way in which we interact with our political class. But a lot of the voters who voted for Donald Trump rejected the Democrats quest for joy. Kamala kept saying, let’s restore joy.

Well, it’s very hard to be joyful when you’re living at the bones, living on the margin of personal insolvency, forced by cost to living pressures and low stagnant income, wage growth and declining services. You’re forced to a very mediocre life and a very high pressured life. So they bought the Trump message.

So I’m not sure they’re the ones you’re referring to that are scrambling to look after their future in the face of what Elon Musk and his mates might do to the bureaucracy.

My feeling is that they still live in hope that Donald Trump will restore the industrial heartlands in the [Great] Lakes District, et cetera, and will get rid of illegal entrants to the country who are deleting the welfare system or whatever. You know, all of those narratives, right?

But I think what is very scary, and this is taking an MMT perspective, is yes, you might argue and hold the view that the spending on the Department of Environment [EPA] and the spending on the Department of Education, all those salaries, are just a total waste of money. But in saying that you will say that you prefer that spending to be elsewhere.

Because if you then say, oh, we can do without all of that government spending, then you’ve got a problem with what’s going to replace it.

Because if you don’t replace it, then the level of economic activity and employment levels will fall and unemployment will rise and poverty will rise.

So even if you don’t like what the government’s spending its money on currently, it is spending that money into the economy and that’s producing jobs.

Now, you might not want those jobs to be where they are, but I see nothing in what Musk and those characters are sort of intimating to suggest that they’ve got the slightest macroeconomic understanding. Spending equals income. And if you cut that spending, well, then what are you going to replace it with?

Because if you don’t replace it with something else more to your ideological preference, then you’re going to have a massive recession. And I think that’s the missing part of the debate at the moment. Yeah, I can accept that.

A lot of Americans think that the Department of Education and the Department of Environment programs are a waste of money and they don’t like them and they would prefer them not to be there. But they’ve got to have something to replace them, otherwise you have a spending collapse. And that’s the missing link in the debate at the moment.

That’s what I think is scary that those guys don’t really have a clue about macroeconomics, and they’re going to feel very warm and fuzzy as they carve up the public sector and get rid of workers in the Bureau of Labor Statistics and Department of Employment and all of those other things that they hate. But I don’t see that they’ve got a plan to replace it other than to continue to feed their mates in the military industrial complex.

That’s my observation.

Steve Grumbine

00:58:18.618 – 00:59:06.510

Well, I think that this kind of ties into the second part of that question about private banks, because when there is, if you look at the sectoral balances and we. I don’t want to dive too far down that runway, but the reality is, is that that money’s got to come from somewhere.

And I guess they’re looking over there at disposable income and they’re saying, hey, good way to get rid of all that excess cash in people’s pockets is to make them go into private debt. And the private banks are there to accommodate that. You know, that is one way.

You know, you got federal spending, you’ve got imports or exports, I should say, as another means of bringing cash into the equation. And then you got private banks, people taking out loans to fill the void that neoliberalism or this slash and burn approach puts them into.

Bill Mitchell

00:59:06.810 – 01:02:16.670

One of the successes of the neoliberal era, which really became apparent as we entered the global financial crisis, was that the first strategy was to suppress the ability of workers to enjoy wages growth in line with productivity growth.

Now, during the 1960s and 70s, in almost every country, the real wage, the purchasing power of the workers wage, grew in proportion with productivity growth, productivity being the grossing output per unit of input. In other words, we’re able to get much more output for a given level of input than we could 20 years prior.

Now, the reason why real wages have to grow in proportion to productivity growth, which they really haven’t since the 1980s, is because of a realization issue that if you’re producing more and more stuff, then how are you going to consume it and sell it and make profit from it? So the first part of the story was to suppress real wages growth and redistribute more cash to profits. That was the first part.

But then you had to work out, well, if you’re going to do that, how are you going to ensure that those redistributed profits are actually realized through sales of goods and services? Because ultimately the capitalist class has to sell stuff to make profits from the services, otherwise they don’t.

And the characteristic innovation of the neoliberal period was to solve that problem by deregulating financial markets and abandoning financial oversight of the financial sector and letting the greed run wild. And so they worked out that, well, we don’t have to pay the workers to consume, we can enslave them in debt and make money off them two ways.

One, by suppressing their wages growth and then making money off interest rates on debt we push onto them. And so, you know, in Australia in the 1980s, you just get this massive invasion in the Daily Mail.

Credit cards being issued to 4 year olds and 10 year olds. You know, their banks went crazy under deregulation.

And what you saw in Australia was household debt as a percentage of disposable income in the 1990s was about 60%, approximately. Now it’s close to 200%.

And that was perfect because the capitalists could suppress your wages growth, but then still sell all the stuff through credit.

Now the only problem with that strategy, which the GFC [Global Financial Crisis] exposed, is that it’s finite because while the government can have as much debt as it ever wants, it issues the currency, the non government sector can’t. And the non government sector will eventually get to a point where it’s too precarious to keep borrowing, and so then they’ll stop spending.

At that point, you have financial recession, bankruptcies, and all sorts of chaos.

So, yeah, for a short time, you can fund growth through private debt increases, but that’s finite and is unsustainable and leads like the GFC to crisis.

Steve Grumbine

01:02:17.060 – 01:02:22.412

I think that’s what we saw in the Bill Clinton era as he slashed and burned the government.

Bill Mitchell

01:02:22.596 – 01:02:23.372

Absolutely.

Steve Grumbine

01:02:23.436 – 01:02:29.708

They had the “Goldilocks economy” because everybody was deep in debt and they were all loving it until the bubble burst.

Bill Mitchell

01:02:29.804 – 01:02:32.428

Absolutely. All around the world it happened.

Steve Grumbine

01:02:32.524 – 01:02:47.636

Absolutely. Well, Bill, I want to thank you for taking us through this. I hope that my questions didn’t come off as stupid.

I was trying really hard to ask what I thought were good questions. Is there anything that I missed that you think would be pertinent to this conversation?

Bill Mitchell

01:02:47.788 – 01:03:05.316

We could go on all day talking about this stuff, but in the interest of brevity, I think we’ll call it quits. I think that the sort of issues you articulate are the issues that people are talking about, and I hope I provided some perspective on them for you.

Thanks very much.

Steve Grumbine

01:03:05.388 – 01:04:08.170

Absolutely. All right, folks, my guest, Bill Mitchell. Friend, thank you so much. I appreciate you, sir. My name’s Steve Grumbine. I’m the host of Macro N Cheese.

We are a very small nonprofit. We need your help. It is a 501c3 in the United States, and that means your donations are tax deductible.

Please consider becoming a donor if you find the material that we produce worthwhile. And with that, like to thank my guest one more time, Bill Mitchell. On behalf of Macro N Cheese and Real Progressives, we are out of here.

Extras links are included in the transcript.

Related Podcast Episodes

Related Articles

The Truth About “Printing Money”

The Strategic Activist

Leave a Comment

You must be logged in to post a comment.