Did you know that the government can never run out of money, taxes don’t fund its spending, the national debt isn’t a debt, and printing money doesn’t cause inflation? Probably not, because your parents, teachers, politicians, and favorite journalists have always told you the opposite.

For most of my life, I didn’t know either. I have two PhDs, and if one of them were in economics, it wouldn’t have helped. The only people who know how government finances work are central bankers (who won’t tell you), traders with hands-on experience of the failure of economic norms, and those who stumble across their work (which I explain below).

Everyone else, from New York Times economists to the leaders of both major parties, reinforce common falsehoods, which may be why the economy is brutal and crashes every ten years. Some of these experts lie, others don’t want to rock the boat or jeopardize their careers, but most don’t have a clue.

That is why, if there is a conspiracy to stop us learning “why the government can never go broke,” for example, so that we don’t ask for nice things like public healthcare, climate action, and a basic income, it is almost effortless. Most people automatically treat the government like a big household that is subject to the same financial rules as themselves—balance income with spending, save for a rainy day, and avoid debt.

As responsible adults, that is our lived experience—the hard truth of budget living that accompanies adulthood—and it continues to guide every financial decision we make. When analogized to the government, disagreement appears infantile to us “adults in the room” who assiduously calculate how to pay for government programs with taxes and cuts.

What eventually caused me to stop basing my beliefs on assumptions, hearsay, and intuition were questions like “where does money come from?” And, how did the trillions of dollars that exist today actually get here? My intuition had only supported the ridiculous notion that money is an eternal object that circulates in the economy and cannot be created or destroyed.

In my examination of what seemed like a scholarly question, I discovered what may be the greatest cause of suffering in the developed world— politicians who falsely declare that a government “cannot afford” something or has “reached its debt ceiling” are creating opposition to social spending that would save lives and could save the planet we live on.

The remainder of this article will provide you with the knowledge to reject their misinformation and, I hope, facilitate the greatest societal change of the 21st century.

Where Does Money Come From?

Take the United States as an example. Every U.S. dollar in existence was created by the U.S. government (or by banks with government licenses), and this exclusive right to create the dollar is enshrined in the U.S. Constitution. It is even called a Federal Reserve Note to tell you it was created by the government’s bank.

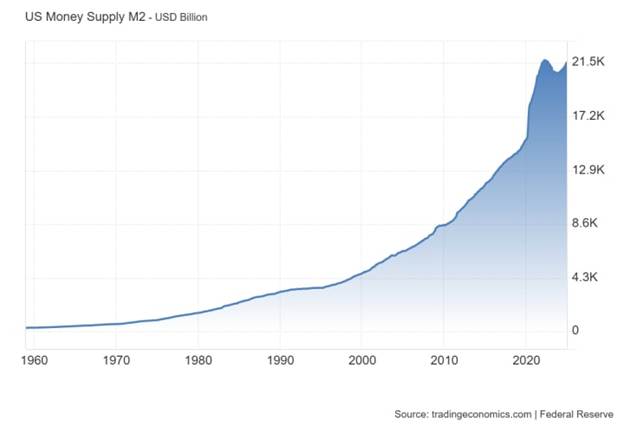

The first dollar was created in 1792 and trillions have been created since then. In fact, there are twice as many dollars in existence today compared to ten years ago (see graph). Although much of the new money is bank credit, the rest is created when the government passes spending bills.

Most national governments are currency issuers, including the U.K., Australia, and Canada, although some are not (e.g., European Union states such as Greece). Localities such as U.S. states also do not create currency and require some form of income.

This power to issue currency means that every statement from a politician, economist, or media personality about the government “running out of money” or being “unable to pay its bills” is a lie.

The Government Can Never Go Broke

In a rare and unreported admission, the Federal Reserve confirmed that the U.S. government issues the dollar and can never run out.

As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. — Federal Reserve Bank of St. Louis

Alan Greenspan also said the following under oath in front of Congress (see video for context).

There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. — Alan Greenspan (Federal Reserve chairman, 1987–2006)

Another Fed chairman, Ben Bernanke, said something similar when he described how the government bailed out the banks after the 2008 financial crisis (see video below). As I said in the introduction, central bankers know how it works. They just almost never tell you.

Taxes Do Not Fund Spending

In the previous video, Bernanke explained that tax money was not used to bail out the banks, and, logically, a currency-issuing government does not need taxes to fund itself.

On a practical level, economists who have studied the operations of the central bank know this to be true.

The proceeds from taxation and bond sales are technically incapable of financing government spending […] modern governments actually finance all of their spending through the direct creation of high-powered money. — Professor Stephanie Kelton

It makes no practical sense for governments to wait until they have accumulated enough in taxes. Or did you think the Treasury was waiting for your grandmother’s taxes to arrive before they could buy a warship?

Rather, they create money as they spend. As Bernanke explained, the government makes a payment by instructing the Federal Reserve to increase the number of dollars in a bank account. This happens by keystrokes on a computer. It doesn’t even need to be printed.

Taxes Are Deleted

There is a veiled admission from the Federal Reserve about the fate of our taxes. Essentially, they acknowledge in footnote 1 here that taxes paid to the U.S. Treasury are no longer part of the money supply (i.e., deleted).

Governments create money by spending and extinguish it via taxation. — Professor James K. Galbraith (former executive director of the Joint Economic Committee of Congress)

Why Tax At All?

Unfortunately, taxation is necessary. When the government creates dollars, it needs you to value and accept those dollars as payment for your goods and labor. The government does this by forcing you to pay taxes only in dollars, which means that you have to obtain dollars from somewhere.

In other words, giving value to the government’s currency is the core reason for taxes, but there are other reasons, such as to reduce the money supply and to punish problematic industries (e.g., polluters). Funding government spending is not one of the reasons. Indeed, governments have to create and spend money before anyone can even pay their taxes.

Printing Money Does Not Cause Inflation

Intuition tells us that creating money reduces its value by the same amount, but this leads to the ridiculous notion that the first dollar ever created was as valuable as the collective trillions in existence today. It also forgets that the money supply is increasing all the time, usually without noticeable inflation.

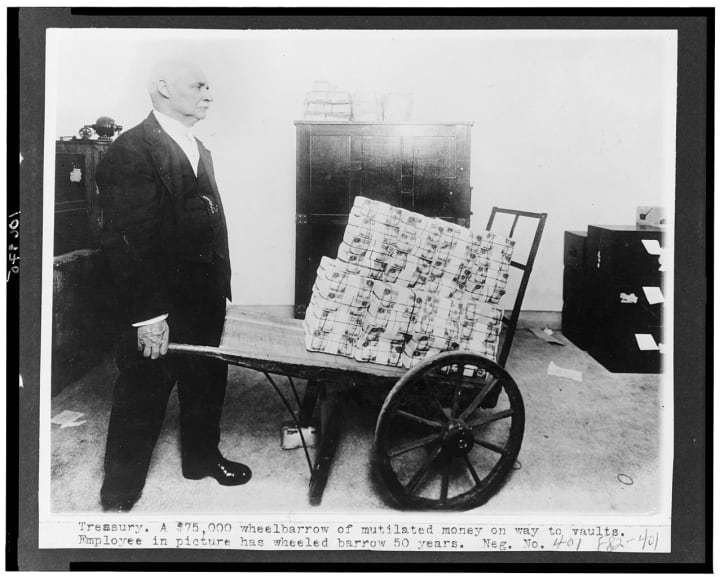

In my case, I held this myopic belief about inflation because I saw a photograph of a wheelbarrow of money in a 7th grade history class about Weimar Germany and I assumed that correlation means causation.

The conventional wisdom that printing money causes inflation is not true. — Professor John T. Harvey

Although money creation could expedite inflation, it was not the cause of the historical examples that most people cite, such as Weimar Germany and Zimbabwe. Rather, the inflation was caused by supply shortages, or foreign debt, and money was created after to maintain the public sector.

The causation is that inflation increases the nominal need for cash and reserves, not that increased cash causes inflation. — Warren Mosler (hedge fund executive and professor of economics)

We can describe inflation with the equation, MV = Py. While increasing the money supply (M) could increase prices (P), the money may be saved, reducing the rate of spending (V). Alternatively, if the money is spent, businesses will seek to accumulate it by hiring workers and producing more goods and services (y). In either case, prices do not increase.

Inflation can occur if there is a lack of resources or labor, which is why it’s usually a supply issue, and why quintupling the money supply in the past thirty years has not brought about Armageddon.

The National “Debt” Is Not Debt

A national “debt” of more than $35 trillion sounds scary. So scary that people are paid great deals of money to tell you how scary it is. The more afraid you get, the less likely you are to want public healthcare or climate action. How could we possibly afford that?

Much of this “debt” is Treasuries, which are savings accounts with the U.S. government that earn interest. Countries like China and Japan buy Treasuries because they earn dollars through trade and have nowhere better to put them. What this tells us is:

- Holders of U.S. “debt” do not want it repaid for the same reason that you don’t want your bank to close your savings account.

- The government does not need the money. It creates all that it needs, and it created every dollar that has since been used to buy Treasuries.

- If the government wants to eliminate this “debt” it can phase out Treasuries and deposit the money into checking accounts.

- If anyone wants to withdraw their money, the government can create/print the withdrawal amount and give it to them (see video).

So the national “debt” is not a debt. When the government creates money, it offers people the chance to buy Treasuries of equal value. These Treasuries, plus cash left in the economy, are the money supply (the total of every budget deficit in history). Eliminating it, such as with less spending and more taxation would eliminate the money supply.

Nevertheless, fear-mongering about the “debt” has persisted for at least 88 years, when it was a thousand times smaller (see video). Normally, when someone predicts the apocalypse, they are discredited when their prediction fails.

Budget Surpluses Cause Recessions

A budget deficit occurs when the government has created and spent more money into the economy than it has removed in taxes. A budget deficit therefore puts more money into your pocket than it takes out.

A budget surplus occurs when more money is taxed out of your pocket than is spent in. This is not good for you, and it doesn’t help the government either because taxes are not saved. But that doesn’t stop corrupt politicians from appealing to popular intuitions about “saving for a rainy day” or the fact that surplus sounds positive and deficit sounds negative.

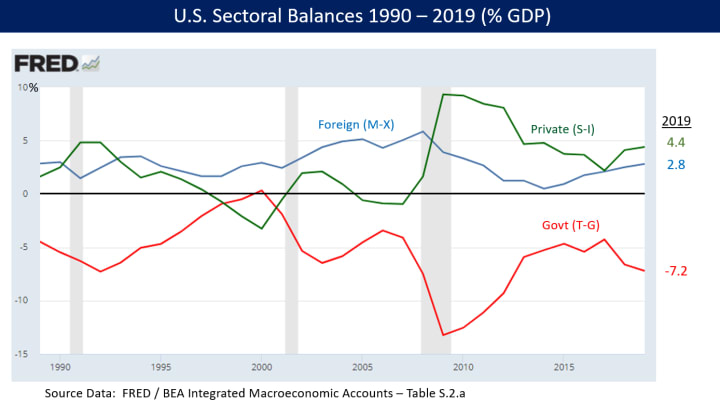

Politicians do this to discourage social spending. Furthermore, attempts to “balance the budget” or have a budget surplus cause cash-strapped people to accumulate private debt (i.e., realdebt) that is held by the wealthy donors of these politicians. Unfortunately, this situation (see graph when the green line drops below zero) almost always triggers a recession (shaded areas of the graph).

Historical data shows that a government deficit (the red line, below zero) is a private sector surplus (the green and blue lines, above zero). Basic accounting tells us that the lines balance out every year and sum to zero.

Why Learning Economics Is Important

Every time a policy is proposed that could save lives, such as public healthcare or climate action, it is belittled with the following eight words: “how are you going to pay for it?”

Liberals propose taxes or cuts that conservatives disagree with, and the two sides have argued about these imaginary financial constraints for decades while millions have died.

The truth is that the government has no financial constraints. It only has resource constraints and the risk that its spending might cause a demand for resources that exceeds the economy’s productive capacity (inflation). However, there is nearly always room to expand that capacity with construction, imports, education, and innovation.

In recent years, Modern Monetary Theory (MMT) and its advocates have popularized and informed people about the ideas presented here. Eventually, these ideas could transform society, causing it to focus less on the importance of money and more on what can be achieved with the real resources at its disposal.

It is no coincidence that every modern historical triumph, from reaching space to winning WW2, acknowledged the triviality of money. We did not say “we can’t afford to fight Germany.” Rather, we looked at what we could do with the resources we had and used money to incentivize people to contribute. A government can create as much incentive as it wants.

In my view, our collective understanding of these paradigm-changing ideas will bring about the greatest societal change of the 21st century. The imaginary financial constraints that our leadership class places upon itself will be removed. Instead of “we can’t afford that” we will say “how do we resource that?” and reduce suffering on a massive scale.

Of course, MMT already has its critics. Typically, they either do not understand the theory or do not want you to understand it. They create straw man versions to make it appear unreasonable, uncomplicated, and not the work of highly-credentialed academics and economists.

For example, you may have heard that MMT is “just about printing money,” that the theory does not consider inflation, or that it can only work while the dollar is the world’s currency (the framework applies to any currency-issuing nation).

Many of these critics have careers or ideologies that have been sustained by their support for economic models that cause a recession every ten years. Other critics have reservations about what will happen to human society if these ideas become popular. Others are wedded to conspiracy theories that impede their ability to process the information.

Dispensing with the intuitive economic falsehoods that you have grown up with should not be entrusted to people whose careers or egos are sustained by them. Rather, MMT should be learned from the academics who developed the theory, such as those listed below.

Sources

- Kelton, S. (2020). The Deficit Myth: Modern Monetary Theory and How to Build a Better Economy. John Murray.

- Mitchell, W., Wray, L. R., & Watts, M. (2019). Macroeconomics. Bloomsbury Academic.

- Wray, L. R. (2022). Making Money Work for Us: How MMT Can Save America. Polity.

Republished with permission from author – original post.

Leave a Comment

You must be logged in to post a comment.