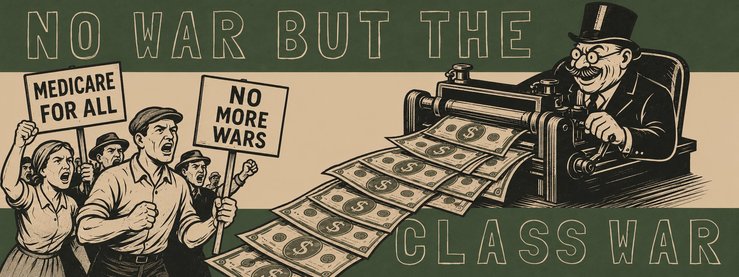

Our lives and livelihoods are being threatened in the direst of ways on a daily basis, camouflaged in the opaque language of financial and economic jargon. Every tv channel and newspaper features some big brain discussing inflation and talking about the economy “running hot” and the need to “curb demand to bring down prices”. The translation of this word salad is that they think inflation is caused by you, the average American who can’t afford $400 for an emergency, having entirely too much money in your pocket. They believe that if you just have less to spend, prices will come down. The problem with that, aside from the obvious stupidity and gross misdiagnosis of the sources of inflation, is that it will fail spectacularly and may even place the future of the country in jeopardy.

In the real world there are things we want and things we need. The things we need don’t become less necessary because the price changes. Food, housing, gas, transportation and utilities are things we need; they happen to be what is driving the current inflation. The only way to drive down demand for those things is to remove people’s ability to survive, and that is exactly what is being casually embraced by politicians and pundits. Historically, this method of governing has ended very poorly for the existing power structure.

The fundamental problem with this approach, as well as the moral repugnance of it, is obvious. “Price elasticity of demand” is what economists call the degree to which demand responds to changes in price. Things like big screen TVs and designer clothes respond quickly to changes in price because you can choose to buy them later, or buy something else instead. Things that people need regardless of whether they cost too much are called “inelastic” because they lack this quality. Healthcare is a fine example of totally inelastic goods or services. If you are having a heart attack, you need to go to the emergency room and have a procedure whether it costs $5 or $50,000. This clearly creates perverse incentives and a situation every bit as coercive as armed robbery. It allows private actors to issue an ultimatum: Your money or your life. Pharma giants often speak of pricing their products “as high as the market will bear.” The scam is that this is not a market, it is a hostage situation. While few things are as totally inelastic as healthcare, the fact that people stubbornly require certain things to stay alive regardless of employment or financial status creates power differentials that render invalid many of the assumptions that economists take as articles of faith. This is brutally obvious to most people who experience it daily. But the smart sounding pundits and experts we’ve been deferring to for too long live in a world of fairy tales, superstitions, and groupthink. Assuming that they know what they are doing is a dangerous mistake.

According to the Consumer Price Index, our official yardstick of inflation, the primary drivers of our persistent high numbers are precisely these sorts of inelastic necessities. Energy, transportation, shelter and food are amongst the things we need to survive. They have a demand floor, a level below which they cannot go without ruining or ending people’s lives. Some individuals may have the option to drive less, but the food at the grocery store still has to be delivered by trucks that run on gas and diesel. There is a minimum demand for transportation fuel that the country cannot dip below if people are to survive. This also helps to push up the cost of food and other goods. People can alter their diet somewhat, but they must have nourishment or they will sicken and die. This puts a floor on demand for food. The connection between food and transportation fuel costs creates a dangerous feedback loop that can only be remedied on the supply side of the equation. Other basic necessities like housing, electricity, working means of transportation, and healthcare also have demand floors for similar reasons. Just as with fuel and food, the price issues can only be addressed on the supply side. To suggest that these are somehow in the same category as big screen televisions, gaming consoles, and designer handbags is obviously ridiculous. To suggest that demand will respond to the same price signals is insanity. Yet that goes unchallenged daily on cable news and major print outlets, as well as in the halls of power.

When former Treasury Secretary Larry Summers or current Fed Chair Jerome Powell talk about driving down demand for necessities and “cooling off” the economy, we need to understand what they mean. They are talking about inducing mass layoffs, driving down wages, and cutting off the means of survival for millions of people. They tried this in the 1970s and 80s with disastrous consequences, but eventually the supply side problem resolved itself and the economy began the slow process of recovery. These measures did not bring down prices as they were expected to because the demand for necessities was inelastic, so suppliers had no incentive to reduce prices. The economy is far less resilient now than it was then. The ripple effects of mass layoffs will spread farther and faster than they ever have before. These include mass foreclosures, mass debt defaults, mass financial collapse, drops in demand for non-essential goods. These will trigger a wave of further business closures and layoffs, and the cycle will repeat because unemployed people have no money to spend. This is called a deflationary spiral, which is the feedback loop that kicks off a recession or depression. As with the 2008 crisis, the financial contagion will likely spread rapidly throughout an interconnected world. When millions upon millions of people become homeless and hungry through no fault of their own and find themselves powerless to provide for their own survival, they eventually start asking what caused this and who is to blame. This creates conditions that lead to state failure, civil unrest, and revolution.

The brain rot that allowed the sorts of charlatans who could believe something so utterly stupid to reach heights of power has a long and complicated history. A host of pernicious self-promoting economists insinuated a great deal of quackery into common discourse over the course of many decades. Schools of business and finance and the scam of “management science” did the same from a different angle. The factor that made all the other corruption in the system possible is the fact that the public accepted the idea that these issues were for “experts” and that these affairs are too complicated for ordinary folks. They accepted as gospel truth that we should all trust these highly competent professionals who obviously absolutely know what they’re doing. But they do not necessarily know what they are doing, and often have considerably less common sense than the average working adult lay person. We cannot afford to go through life refusing to check under the hood even when we hear an ominous knocking sound within. Through neglect this confederacy of dunces has gained power by pandering to power and in the process manipulated the discourse to marginalize more sensible views and create the false impression that their views are the only options on the table. Frauds and hucksters have always relied on false dichotomies and thought-terminating cliches to misdirect the attention of their audience from more appealing alternatives. In this case the options in question make far more sense given that we know very well the sources of the problems lie in things like the fragility of supply chains and perverse incentives from monopolists and the financial sector. A vast and flexible array of tools exist to combat inflation on the supply side, some of which have been in use for thousands of years.

A frequently mentioned intervention of late is price controls. This is actually not a singular policy but a whole array of menu options, some of which are quite gentle and market-friendly while others are more heavy-handed. The sophisticated types of price interventions under discussion include the use of government asset purchases for strategic stockpiles called “buffer stocks” that can be added to or released into the market to “collar” prices when they get too high or too low. These are relatively light-touch short-term interventions that can curb price gouging and remove perverse incentives to keep prices high by speculators and producers. They also provide a flexible kit of tools useful for relatively unobtrusive interventions in global markets to help rectify supply bottlenecks. This can be used to address the situation right away while longer-term projects like antitrust enforcement get underway. Other short-term measures like punitive taxation and light touch versions of targeted capital controls can be utilized, but they will not eliminate the systemic and structural problems that got us here. Even antitrust enforcement, while necessary, is far from sufficient.

A glaring source of structural problems is the introduction of private profit motive and “the market” where it does not belong. Solutions must be considered to de-commodify or at least strictly regulate the most inelastic of essential goods and services. It makes no sense, after all, to trust the market to allocate goods that do not respond to market forces. Robust government intervention to regulate the behavior of private actors in these spaces are necessary. Ranges of options exist from subsidies and punitive taxation to tighter regulation as public utilities to full nationalization. Eliminating the vast waste and inefficiency that comes from misdirected incentives and coercive extraction would have profound counter-inflationary effects, potentially requiring additional government spending to prevent overcorrection from job losses in predatory sectors. Investment in public infrastructure and productive capacity is an ideal way to counter that problem while increasing resiliency against future price shocks. The government need not fear debts and deficits when funding is directed at targets that promote productive capacity and price stability. The quantity of money is largely irrelevant to inflation; it is where it is going that matters. There are many and varied viable ways of achieving these ends, but the important thing is the commitment to achieving outcomes in the public interest, regardless of what is best for the bottom lines of capital and finance. Taking a forceful and adversarial role against private actors in spaces like transportation, housing, oil refining, and the distribution of foodstuffs will be necessary from a government that has long been allergic to confronting or rebuking the donor class. Elected officials are just going to need to take an antihistamine and get comfortable with that.

The inflationary devil whose name is never spoken aloud in mainstream circles is the finance sector itself. A paper in the American Affairs Journal by Julius Krein lays out a fairly damning indictment with numerous receipts. The finance sector has been cannibalizing the real economy for decades now. As a result, nearly all the assumptions of the so-called mainstream economists have been rendered invalid. Not only are corporate revenues now completely detached from real economic growth, but stock valuations are even detached from corporate revenues. Oil and gas companies, for instance, have found they can boost their stock value by skipping the profits from investment in increased capacity and focusing on “financial innovations” instead. The world of major banking institutions, as well as the shadow banking sector like private equity and hedge funds has come to resemble a series of financial shell games rife with self-dealing, perverse incentives, and fuzzy accounting. A great many pernicious innovations of recent decades have arisen from the financial engineering driven by the focus on maximizing shareholder returns. The outsourcing of everything productive, the drive to reduce or eliminate labor costs (i.e. someone’s income), the increasingly precarious and unnecessarily distributed supply chains and the rise of an increasingly rentier driven economy are just a few examples of such developments. The increasing financial complexity associated with the cannibalization of the real economy is designed to undermine normal economic patterns and rig the rules in favor of financial elites, as predicted by heterodox economists. It also insulates a major driver of inflation from the whims of supply and demand and other market forces, rendering attempts to suppress demand utterly impotent and setting the stage for the next crisis.

Prominent economic opinion makers repeat ad-nauseum that such changes are irreversible, and that we must learn to live with them. The people making these claims are as often as not the engineers of such developments. Former Treasury Secretary Larry Summers is a prominent example, and his own conflicts of interest are typical of the loudest voices in policy and opinion making circles. Summers has had a hand in some of the most spectacular worldwide financial disasters of the last half century, and has played no small role in the development of the current state of affairs. He was, to cite a glaring example, one of the foremost champions of the removal of the last vestiges of depression-era guardrails on finance, unleashing a pandora’s box of evils into the world. He is part of an illustrious tradition of arrogant economists and politicians insisting that their destructive and self-dealing innovations are inevitable and irreversible. Larry even goes so far as to call those who suggest otherwise “economic luddites”. But these things are not irreversible. We have been here before, and they were eventually reversed. The cost to learn those lessons was astronomical, and the consequences of initial failures were terrible. It would be twice the tragedy if we failed to learn from their experience.

Addressing the current inflationary crisis is easy if the government is willing to act, and to disregard the advice and inclinations of self-interested parties peddling catastrophic policy prescriptions. The heavier but no less essential lift is altering the structural rot that makes a recurrence of these conditions inevitable. The financial sector must be put back in its cage and secured with newer and more robust guardrails. The euthanasia of the rentier state must be a feature of state policy, not a bug. The natural decline or even elimination of the shadow banking sector such as hedge funds and private equity firms must be actively assisted, and such social parasites must be denied access to critical goods and services like housing, healthcare, and energy. Essential and inelastic goods and services must be de-commodified and protected from price fluctuations and supply shocks. National single payer healthcare and Austrian style public housing are within easy reach of an economy as powerful as that of the United States of America, if we are willing to commit to it. The most important thing to commit to is unceasing and eternal public vigilance. When we leave the so-called “experts” and other interested parties unsupervised, the interests of honest people are under threat. The only way these will be upheld and secured in perpetuity is if we come together to insist upon it, never again to relent.

Leave a Comment

You must be logged in to post a comment.